Originally published September 2018. This Update incorporates the latest CBO and trustees report data.

Back in September 2018, I wrote a blog post asking whether Social Security was going broke. At the time, the Social Security Board of Trustees was projecting the trust fund would be depleted by 2034 — at which point benefits would be cut to about 79% of normal. Nearly eight years have passed. So how has the picture changed?

The short answer: it's gotten worse — and faster than many people realize.

The depletion date has moved closer — and Congress has made things worse

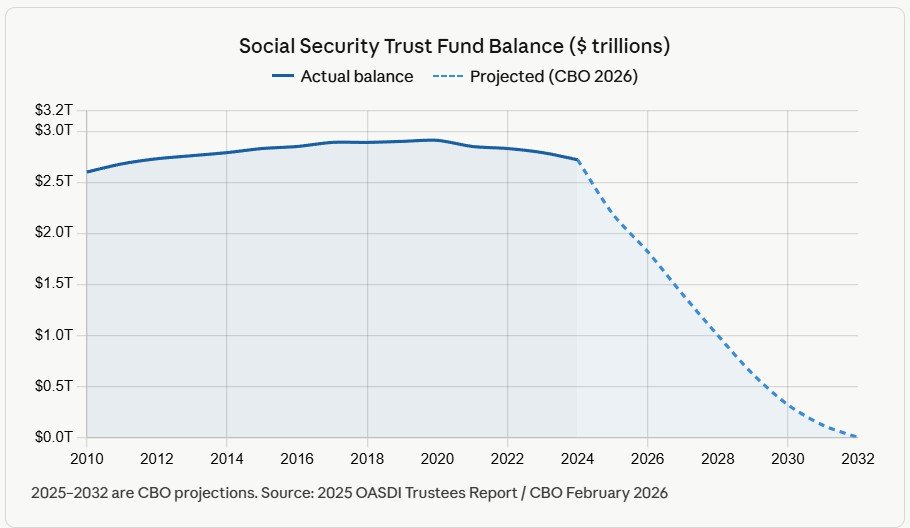

When I wrote that 2018 post, the trustees projected depletion of the combined trust funds by 2034. The most recent Social Security Trustees Report (released June 2026) accelerated the trust fund’s depletion date to 2032 — two years earlier than prior projections just a couple of years ago.

Why did the date move up so quickly? Three forces converged:

The Social Security Fairness Act (Biden, Jan 2025) eliminated the Windfall Elimination Provision, increasing benefit payments

The One Big Beautiful Bill Act (Trump, May 2025) introduced a new $6,000 senior deduction, reducing taxable benefits income flowing into the trust fund

Higher-than-expected inflation is driving larger cost-of-living adjustments

In other words, Congress passed legislation that expanded benefits without funding them — accelerating the clock.

What does depletion mean for your check?

This is the number that should get your attention. At the point of the trust fund’s projected depletion in 2032 — assuming no Congressional action — retirement beneficiaries would see a 22% benefit cut — roughly a $460 monthly reduction for the average recipient — according to the Committee for a Responsible Federal Budget (CRFB).

It's important to understand what depletion does and doesn't mean. Benefits don't simply stop. At the point of OASI trust fund depletion, continuing program income would be sufficient to pay 78% of total scheduled benefits regardless of need or contribution history. In my 2018 post I cited a projected post-depletion payout of 79% — and unfortunately, that number has become slightly worse.

No state will be spared

The CRFB just released a state-by-state analysis of the impact. The benefit cuts would affect between 10% and 23% of each state's population. "No state would be spared from the potentially devastating effects of insolvency," the committee concluded.

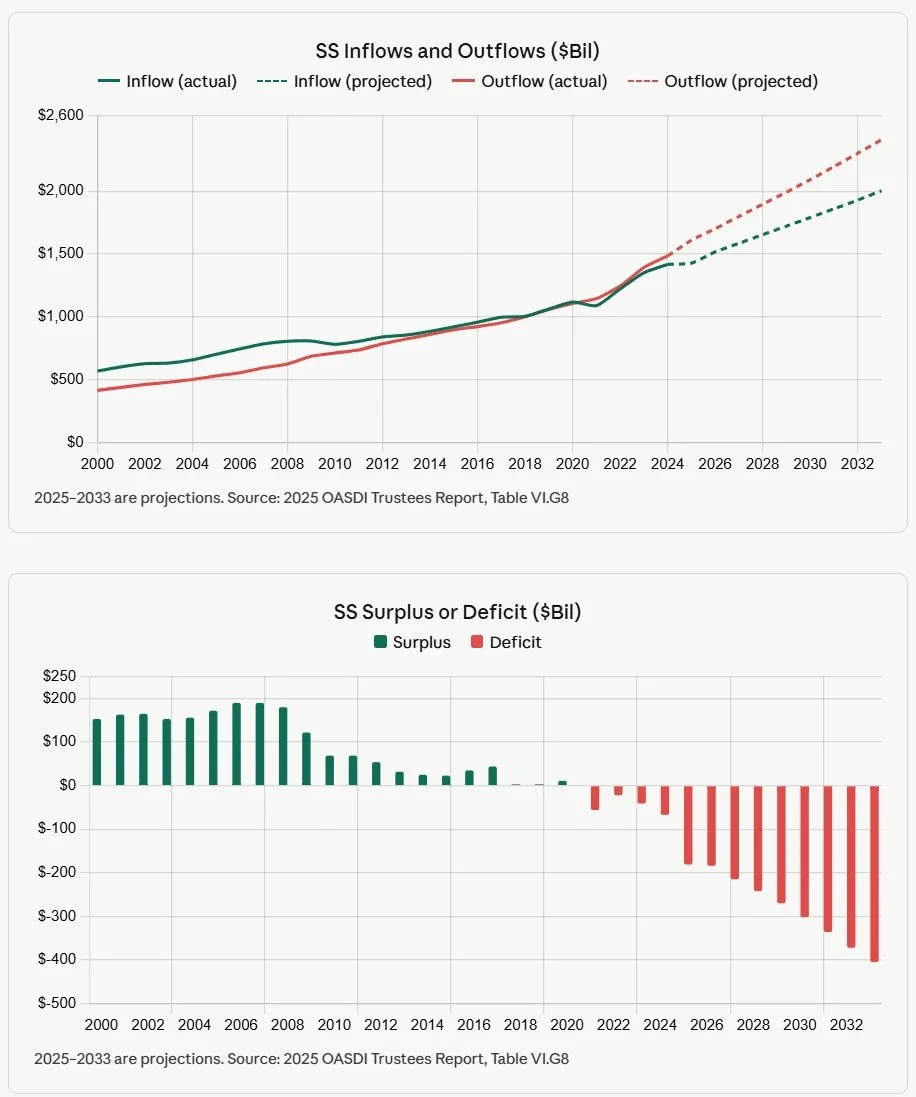

The trust fund will begin to shrink fast

From 2000 until 2009, surpluses totaled more than $120 billion annually, but then steadily declined to essentially $0 by 2020. Assuming Washington does nothing, rising annual deficits from now on will deplete the SS trust fund from $2.2 trillion at the end of 2025 to $0 by 2032.

The math still doesn't work — and it's likely to get worse

In 2018 I wrote that the fundamental problem was primarily demographic: too many retirees, too few workers. That hasn't changed. In fact it's accelerated. We are currently in "Peak 65," a period from 2024 to 2027 in which more than 4.1 million Americans are turning 65 each year — the largest surge of retirements in our nation's history.

The worker-to-beneficiary ratio continues its long decline. In my 2018 post I noted it had fallen from 3.7 workers per beneficiary in 1970 to 2.8 in 2018. That ratio stood at 2.7 in 2023 and is projected to fall further to 2.3 by 2036. Fewer workers supporting more retirees is a math problem that doesn't fix itself.

Has Washington done anything useful?

No, at least not yet, and time is running out. As noted above, the two pieces of legislation Congress passed recently — the Social Security Fairness Act and the senior deduction in the One Big Beautiful Bill — both expanded benefits or reduced revenue without addressing solvency. A plan to actually restore solvency would now require the equivalent of at least a 22% reduction in benefits for current and future beneficiaries, a 29% increase in payroll taxes, or some combination of the two according to the Committee for a Responsible Federal Budget.

This isn't an unprecedented situation — Social Security was just months away from running out of money in the early 1980s before changes were made. The sooner Congress acts to fix the problem, the less painful any changes will be. But Congress hasn't acted, and the window keeps narrowing.

What this means for your retirement planning

The bottom line is the same as it was in 2018, only more urgent: do not build your retirement plan around receiving 100% of your projected Social Security benefit. The smart move is to model scenarios where you receive 75–80% of your expected benefit, or where your benefit is delayed, and make sure your savings can cover the gap.

That's exactly what the Relax Retirement Planner can help you do. You can model "what if Social Security is cut 25%" right alongside your other retirement variables — taxes, market returns, inflation, spending changes, Roth conversions, spousal scenarios — so you know exactly where you stand regardless of what Washington does or doesn't do.

The time to plan for this is now, while you still have years to adjust.